Trucking Liability Insurance

Trucking liability insurance is the coverage that pays when your truck hurts someone else or damages their property. It’s the policy the federal government requires before you can run under your own authority, the coverage your filing is built on, and the one a claim is most likely to draw from. Every motor carrier needs it, from a single owner-operator to a growing fleet.

|

The short answer Trucking liability insurance is third-party coverage that pays for the bodily injury and property damage your truck causes to other people while you operate under your authority. The FMCSA requires at least $750,000 for general freight, though most brokers and shippers want a $1,000,000 limit. It does not cover your own truck or your cargo. |

What trucking liability insurance covers

Trucking liability insurance, also called primary auto liability, responds when you are at fault in an accident and another party is hurt or their property is damaged. It pays them, not you. That’s the whole idea of a liability policy: it protects the people on the other side of a crash so a single bad day doesn’t end your business.

- Bodily injury. Medical bills, lost wages, and legal damages for people your truck injures in an at-fault accident.

- Property damage. Repair or replacement of the other vehicle, plus guardrails, buildings, freight on the other truck, and anything else you damage.

- Legal defense. The cost of defending you when an injured party files a claim or a lawsuit, which after a serious crash is where much of the money goes.

- Your FMCSA filing. The coverage your BMC-91 filing rides on, the thing that keeps your operating authority active.

Liability is the most commonly paid coverage in a trucking claim, and the payout can run to $1,000,000 or more depending on the limit you carry. That is why carriers underwrite it so carefully, and why it makes up the largest part of most commercial truck insurance premiums.

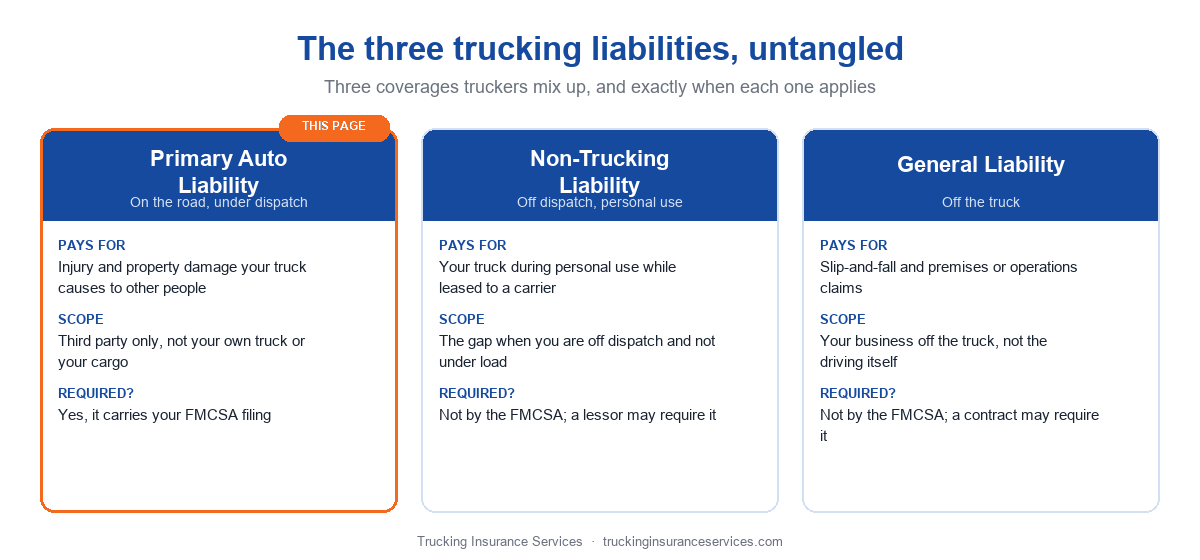

Trucking liability vs non-trucking liability vs general liability

This is the part owner-operators get wrong more than any other, and the search results do not make it easier because the three coverages get blended together. They aren’t interchangeable. This is how we explain the difference to the truckers we insure.

| Coverage | What it does and when it applies |

|---|---|

| Trucking (primary) liability | The legally required coverage that pays others when your truck causes injury or damage while you are working under your own authority. It carries your federal filing. |

| Non-trucking liability | For an owner-operator leased onto another carrier, this covers the truck during personal use, when you are off dispatch and not under load. It is not a substitute for primary liability. |

| General liability | Covers your business operations off the truck, like a slip and fall at a dock or damage you cause on someone’s premises. It is not auto coverage and does not satisfy your filing. |

The short version: primary liability is what lets you legally operate and haul freight. Non-trucking liability only covers the truck when you are using it personally while leased to a carrier. General liability handles the off-truck side of your business. Many operations need more than one of these, but only primary liability keeps your authority active.

What trucking liability does not cover

Because it’s third-party coverage, liability pays the other party. It does nothing for your own equipment or the freight you’re paid to carry. Those need separate coverages, and leaving them off is one of the most expensive mistakes a new carrier can make.

- Your truck and trailer. Damage to your own rig is physical damage coverage, written as comprehensive and collision. It runs about 3% to 12% of the equipment value; a $50,000 truck is roughly $1,500 to $6,000 a year.

- The cargo you haul. The commodities you are paid to move are covered by motor truck cargo insurance, not liability.

- You and your driver’s injuries. Liability pays the people you hit, not your own people. That is a separate conversation.

How much liability coverage you are required to carry

The legal minimum and the practical minimum are two different numbers. The FMCSA sets the floor, but brokers, shippers, and some states require more before they will give you a load or let you operate. Here are the limits that actually come up.

| Situation | Required limit |

|---|---|

| FMCSA minimum, general freight (non-hazmat) | $750,000 |

| What most brokers require | $1,000,000 |

| FMCSA minimum, Auto hauler | $1,000,000 |

| Hazmat | $1,000,000 to $5,000,000 |

| New Jersey trucking companies | $1,500,000 |

For a deeper look at filings and the rules for new authorities, see our guide to FMCSA insurance requirements.

How much trucking liability insurance costs

Primary auto liability for a single truck at a $1,000,000 limit generally runs $5,000 to $20,000 a year. The spread is wide because the number depends on your equipment, your radius, your driving record, and how long you have been in business. A light box truck on a short local route sits near the low end; a heavy long-haul rig sits near the top.

| Operation | Typical cost |

|---|---|

| Box truck, local or regional | $665 to $1,335/mo ($8,000 to $16,000/yr) |

| Tractor-trailer and long-haul | Up to $1,665/mo ($20,000/yr) at the high end |

| Generic single-truck range | $415 to $1,665/mo ($5,000 to $20,000/yr) |

These are the ranges we see on the policies we place. For a full breakdown of trucking liability insurance cost by truck type, see our cost guide. Your own number comes down to the details, so the only way to know it is to get a quote.

What drives your liability rate

Because liability is where the big claim dollars go, carriers price it on how likely you are to have a serious loss. Two things move the number more than anything else.

Claim frequency will make or break coverage. What an insurer will pay on any one claim is unpredictable. A crash that looks like a fender bender at the scene can balloon into a massive payout once a bodily injury appears later or an attorney gets involved, even when the other party walked away looking fine. So carriers rate on how often you have accidents, not just how bad each one was. Stack up enough claims and the issue stops being price and becomes whether any carrier will write you at all.

Your DOT safety scores heavily impact pricing. Out-of-service events, unsafe driving violations, and especially repeat violations push liability rates up fast. Repeat violations are the big one, because they tell an underwriter you are not fixing the safety problems that lead to crashes. A clean safety profile is one of the strongest levers you have on price.

New ventures pay more, and there’s no way around it at first. With no operating history to review, you’re a blank slate, and the carrier is taking a risk until you build a track record. The good news is that the same record that costs you early on starts working for you once it’s clean and seasoned. These habits bring liability cost down over time:

- Forward-facing dash cams. They prove fault, and underwriters increasingly reward them.

- Continuous driver training and a safe-driving reward system. Both lower claim frequency, which is the number that matters most.

- A good mechanic plus pre-trip and post-trip inspections. Mechanical defects become out-of-service violations, which become higher rates.

- Dispute bad violations through DataQ. An incorrect violation or out-of-service on your record costs you real money, so challenge the ones that are wrong.

Liability keeps your authority active

Most truckers don’t set out to buy liability insurance. They want their MC number active so they can take loads, and the liability policy is what carries the federal filing that keeps that authority alive. Let it lapse and your insurer notifies the FMCSA, your filing comes off, and you can land back at square one as a new venture. Keeping the coverage active without a gap matters as much as the limit you carry. For the limits a new authority needs, see how much insurance you need to activate your MC number. And if a policy ever lapses, here is what happens when your truck insurance lapses.

When you might need higher limits

A $1,000,000 limit has been the broker standard for years, but it isn’t always enough. Final-mile and last-mile contracts often require a $1,000,000 umbrella on top of your liability, and after the 2026 Montgomery Supreme Court decision on broker liability, we expect more brokers to push for higher limits. Excess coverage runs about $4,000 to $6,500 a year per $1,000,000 of added limit, and it is worth a serious look if you run through high-litigation states like Georgia, Florida, and Texas. Get a quote and we will right-size your limits.

Why truckers bring their liability to us

We’re a trucking agency first, so we know which markets actually want a new authority and which ones won’t touch it until you’ve seasoned. That matters with liability more than any other coverage. A new venture has a handful of markets that specialize in writing it, and after two or three years of continuous coverage and a clean record, the preferred markets open up with better rates and stronger coverage. Knowing where you fit today, and where you will fit next year, is the difference between a fair price and an expensive one.

The owner here ran her own trucks before she ever wrote a policy, and that background runs through how we handle compliance and filings. We’ve been licensed since 2007, the same people are here year after year, and we place liability for owner-operators, new ventures, and fleets every day. We work to get you the limit you need, keep your filing clean, and keep you on the road.

Get your free quote → or call 855-281-2924 for a same-day rate.

Frequently asked questions

What is trucking liability insurance?

It is the third-party coverage that pays for the bodily injury and property damage your truck causes to others while you operate under your authority. It is legally required to run, it carries your federal filing, and it does not cover your own truck or cargo.

How much is liability insurance for a truck?

For a single truck at a $1,000,000 limit, primary liability generally runs $5,000 to $20,000 a year. A local box truck is near the low end and a heavy long-haul rig is near the top. Your record, radius, and time in business set the final number.

Is $750,000 or $1 million of liability required?

The FMCSA minimum for general freight is $750,000, but most brokers and shippers require a $1,000,000 limit before they will give you a load. Auto haulers and hazmat haulers carry more. In practice, $1,000,000 is the working standard for most carriers.

What is the difference between trucking liability and non-trucking liability?

Trucking, or primary, liability covers you while you are working under your authority and carries your filing. Non-trucking liability covers an owner-operator’s truck during personal use while leased to another carrier, when you are off dispatch. They are not interchangeable, and personal-use coverage will not satisfy your filing.

Does trucking liability insurance cover my truck or cargo?

No. Liability only pays the other party. Damage to your own truck is physical damage coverage, and the freight you haul is covered by motor truck cargo insurance. Both are separate from liability.

Why does my truck liability insurance keep going up?

Usually claim frequency and DOT safety scores. Repeat violations and out-of-service events tell underwriters your risk is rising, and each new claim raises the odds of a large future payout. Dash cams, driver training, clean inspections, and disputing bad violations through DataQ all help bring it back down.

Do I need a $2 million liability limit now?

Many carriers still operate on $1,000,000, but after the 2026 Montgomery Supreme Court decision we expect more brokers to ask for higher limits, and excess coverage is one way to get there. If you run through high-litigation states like Georgia, Florida, or Texas, higher limits are worth a serious look now.

Figures are estimates based on the policies we place and current market rates, offered for general guidance only. Your actual premium depends on your record, equipment, radius, and limits. Get a quote for an exact number.